What is a good credit score? Have you ever had this question popped up in your mind when you read the requirement for taking a mortgage loan or buying a house? Yes, a good credit score is always there, as one of the requirements for getting you a house. Unfortunately, not many people know and understand what this thing is. So, to help you learn more about credit scores and mortgages, we have this article here for you.

What is a Credit Score?

First of all, you need to know what a credit score is. A credit score consists of three numbers. These three numbers represent your creditworthiness. In other words, it shows your capability in paying your credit. The loan company will use these numbers to determine your risk level as the borrower.

So, whats a good credit score? It is the numbers that show that you have low risk. Thus, you will get loan approval much easier. The higher your credit score is, the better its value. Therefore, you should try to keep your credit score in high numbers to get a better chance in various financial activities.

What Is Considered A Good Credit Score?

What is considered a good credit score for buying a house or applying for a mortgage loan? It depends on the scoring model or system to measure one’s credit score. Yes, there are many of them. Therefore, you will also have many credit scores according to the system you use. However, many mortgage companies use FICO as a reference to see their client’s credit score. So, we will go with that as well.

FICO Credit Score

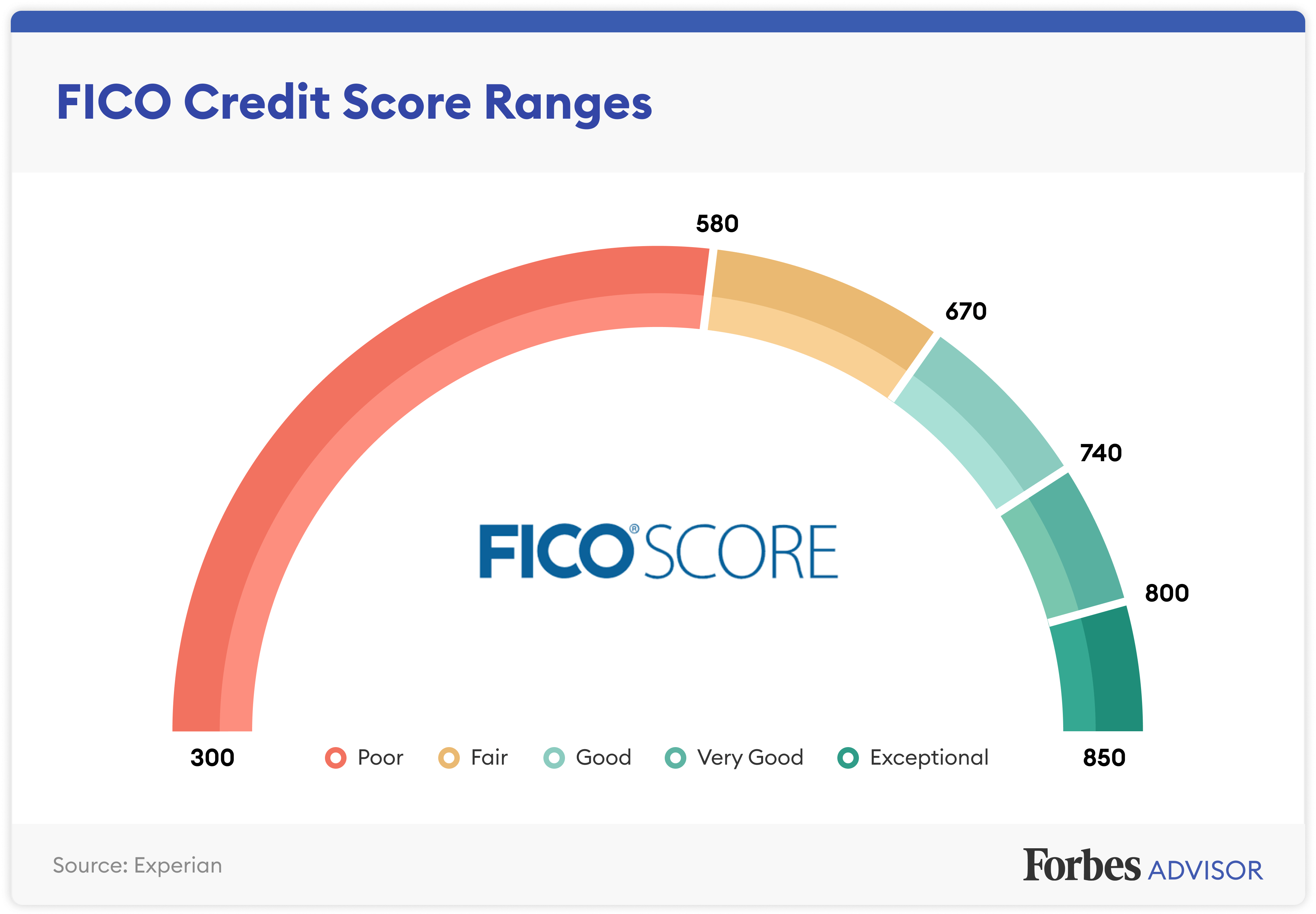

What is a decent credit score according to the FICO scoring system? Here, we will give you a list of the range of credit scores that FICO uses to determine the financial situation and strength of a person. The range is from 300 to 850 and is classified into five categories.

- Less than 580 – people with a credit score less than 580 are considered in a Poor category. It means they enter the risky borrowers’ category. Mostly, the mortgage loan company won’t approve the borrower with this credit score.

- 580 to 669 – this score range is a below-average score, thus entering the Fair category. A borrower with this credit score has a bigger chance to get approval than the Poor category. However, they will be considered unfavorable clients or the last position on the list.

- 670 to 739 – this FICO score is in the Good score range. This score also represents above the national average credit score. So, if you are in this score range, you are in the best condition. You have a better opportunity to get loan approval.

- 740 to 799 – If your credit score is in this range, you have a Very Good credit score according to the FICO scoring model. It is way above the average score. Therefore, as a client, you have very low risk and are trusted to be able to pay off your loan on time.

- 800 to 850 – Exceptional credit score range. This is the category for this credit score range. This score is the best one. You will get approved easily. Moreover, you also have access to various extra features, such as better rates and other bonuses.

Those are the general thing that you should know about the fico score range. The next thing you also need to get is a good credit score for applying for a mortgage loan. We don’t force you to get the Exceptional or Very Good credit score according to the FICO model. You only need to aim for the average FICO credit score to get a better chance for your loan.

So, which fico score do mortgage lenders use? According to data presented by Experian, one of the three major credit bureaus, the average FICO credit score is 716 points. This number is the result of the survey conducted in April 2021. ‘

One thing you should understand, the average credit score needed for home loan has an increasing tendency by 4-6 points from the previous year. So, you also need to adjust your credit score goal every year.

The 716 point here means that the borrowers have fulfilled their obligation without any problem. They don’t have too many late payments, no irresponsible usage of their credit card, and their debt keeps shrinking over the year.

As mentioned before, there is not only one credit scoring model. Other than FICO, you also can find VantageScore. Mostly, VantageScore has a lower score than FICO. It seems easier to reach. However, we recommend you use the FICO credit score for home loan to be safe. By having a higher credit score, you will also have a better chance with your mortgage loan.

How to Find Credit Score for Buying House and Apply for Mortgage Loan

What is a good fico score for a mortgage? After you understand the categories of FICO credit score, you also need to know the best score for applying for a home loan. The 716 points average is a good choice. However, each company might have a different requirement. Some are lower and the others are higher.

Most of the loan companies use the FICO credit score from three major credit bureaus, Experian, Equifax, and TransUnion. Each of those bureaus uses a different FIC credit scoring model, which is:

- Experian with FICO Score 2

- Equifax with FICO Score 5

- TransUnion with FICO Score 4

Each of those types is classified as the classic FICO score system. They are easy to use to measure one’s financial capability regarding loans and debt. So, if you are asking, what is a good fico score, you will get the answer from one of those three bureaus. The answer could be different. What would the loan companies do when they found the different FICO scores from those three major credit bureaus?

According to Darrin Q. English, a senior community development loan office at Quontic Bank, the loan companies will use the median score of those three FICO credit scores from those bureaus. This method is also known as tri-merge.

The loan companies do not take the highest or lower credit scores. They choose the middle score to determine the risk. Moreover, if you apply for the loan with your partner or spouse, their credit score will also be included in this calculation. The loan companies will find the median score from both clients and choose the lowest one. That’s the credit score for mortgage you can use.

What Credit Score Do You Need To Buy A House?

Now, let’s move to the more detailed topic regarding credit score to buy a house. Other than the average FICO credit score, you also can find the minimum credit score you should have based on the loan type. Here are some of them:

- Conventional Mortgage Loan

A conventional mortgage loan is not a government program. This loan only fulfills the minimal requirement set by the government. Therefore, the credit score requirement for this loan is higher than other loans. As for this loan, you need to have at least 620 credit score points. Below that number, you won’t be able to get the approval. Or, the lender could add much higher interest.

- FHA Loan

What credit score is needed to buy a house with an FHA loan? The credit score is lower than the conventional loan requirement. You only need at least 580, the limit of a good credit score according to the FICO scoring model.

FHA Loan is also a good choice if you are a newbie. For the first mortgage loan you apply for, you should use this loan because it is backed by the Federal Housing Administration. This government organization protects the lender from loss when they can’t pay off the loan. Moreover, this loan also has a low down payment. So, use this loan requirement to find a credit score needed first time home buyer.

- VA Loan

VA or Veteran Affairs loan is a government program for veteran or qualified service members. It also works on your spouse. You don’t need a down payment and the requirement is much lighter than other loans. As for the credit score, this loan uses the minimum limit of the credit score, which are 580.

- USDA Loan

This loan is another government program for low-income individuals. However, even though it is made for low-income individuals, you need to have a higher credit score than other loans we mentioned before. For applying for a USDA loan, you need to have at least a 640 credit score. However, you get many benefits from this loan, from low to no down payment, low-interest rate, and other advantages.

What is a good credit score to buy a house based on loan type? From the information above, you can see that the average 716 is the best credit score you can aim for applying for one of those four mortgage loans. However, if that is too difficult for you, the minimum requirement of a USDA loan, 640 points, is enough.

What credit score do i need to buy a house, if I don’t have the minimum credit score requirement? As long as your credit score doesn’t fall below 500, you still have a chance. On the other hand, you should show the lender that you have the capability and intention to pay off your debt, by doing the things below:

- Pay more down payment,

- Paid off your large debt to get a good debt-to-income ratio,

- Save more money in your account (you need to cut down your expense to make this work),

- Have a good employment history (do not make a big mistake in your work and show you have made many achievements),

- Get a co-signer with a good credit history.

At this point, we believe that you understand the answer to what credit score do you need to buy a house question. You also know how to have a better chance to get loan approval with a low credit score. Yet, you still need to fix your credit score, so you won’t have any problems in the future.

How to Fix Your Credit Score

You don’t need to hire a professional to fix your credit score. Yes, the professional might solve this problem easily. But, if you have a tight budget situation, you can do it yourself. Here is what you should need to improve the credit score needed to buy a house.

- Pay your bills on time – this factor affects your credit score the most,

- Reduce the usage of credit cards – keep your credit card balance low. According to some experts, you only need to use less than 30% of your credit card limit.

- Check your credit report regularly – there are many cases where the error of calculation affects your credit score. Therefore, check your credit score frequently to see whether or not the error exists. Then, you can report the error which also improves your credit score.

- Do not close your credit card – closing the credit card will increase the credit utilization and lower your credit score. So, use it occasionally, and then pay it off on time or before the deadline. That will prevent the automatic closing from the issuer because of inactivity.

- Apply for a new credit card – you also can build up your credit history by applying for a new credit card. Choose the secured credit card or credit-builder loan. This method will improve your credit score. However, it doesn’t work immediately. You should apply for it at least six months before you apply for a mortgage loan. That will help you to get the minimum credit score to buy a house.

Conclusion

What is a good credit score to buy a home? We hope this article has all the answers that you need for that question. Now, make some moves, plan your mortgage loan and fix your credit score. You are ready to buy and own a house.