Today, there are many types of loans individuals can access to solve financial difficulties. Home equity loans are one of the most common types of loans and the perfect solution when you need to borrow more money. These loans are generally available in much larger sums than a personal loan, and they can offer you a fixed interest rate that might be better than what you would be able to get from a credit card or a bank. Plus, if you’re a homeowner and you need to borrow money, you may be able to borrow even more than you would be able to borrow with other types of loans.

What is a home equity loan?

A home equity loan is a second mortgage that provides a lump sum of cash for a specific purpose for the homeowner, typically for a down payment on another property. The interest rate on a home equity loan is usually lower than on a first mortgage because the homeowner is borrowing against their equity and not their entire home. The repayment plan usually does not exceed fifteen years but can be extended. The total interest paid will be higher than the interest on a first mortgage over the same amount of time.

How do home equity loans work?

The equity that you have in your home could be an excellent way to finance a large purchase or get the cash you need for a minor purchase. The best way to think about how a home equity loan works is to think of your home as a bank. So long as you keep on paying your mortgage, you continue to build equity in your home, which you can borrow against. You can borrow up to a certain percentage of the equity in your home, and if you want to borrow less than that, there are options to do so. You can borrow up to 80% of the equity in your home or even borrow the total amount that you have in equity if you want to.

Home equity loans allow homeowners to borrow money against their home’s value. This is a beneficial tool for homeowners looking to purchase a new home, pay off a large debt, consolidate debt, or make home improvements. A home equity loan is a loan that you can take out against your home. It’s similar to a second mortgage. These kinds of loans allow you to borrow money against your home’s value. Home equity loans are a beneficial tool for homeowners looking to purchase a new home, pay off a large debt, consolidate debt, or make home improvements.

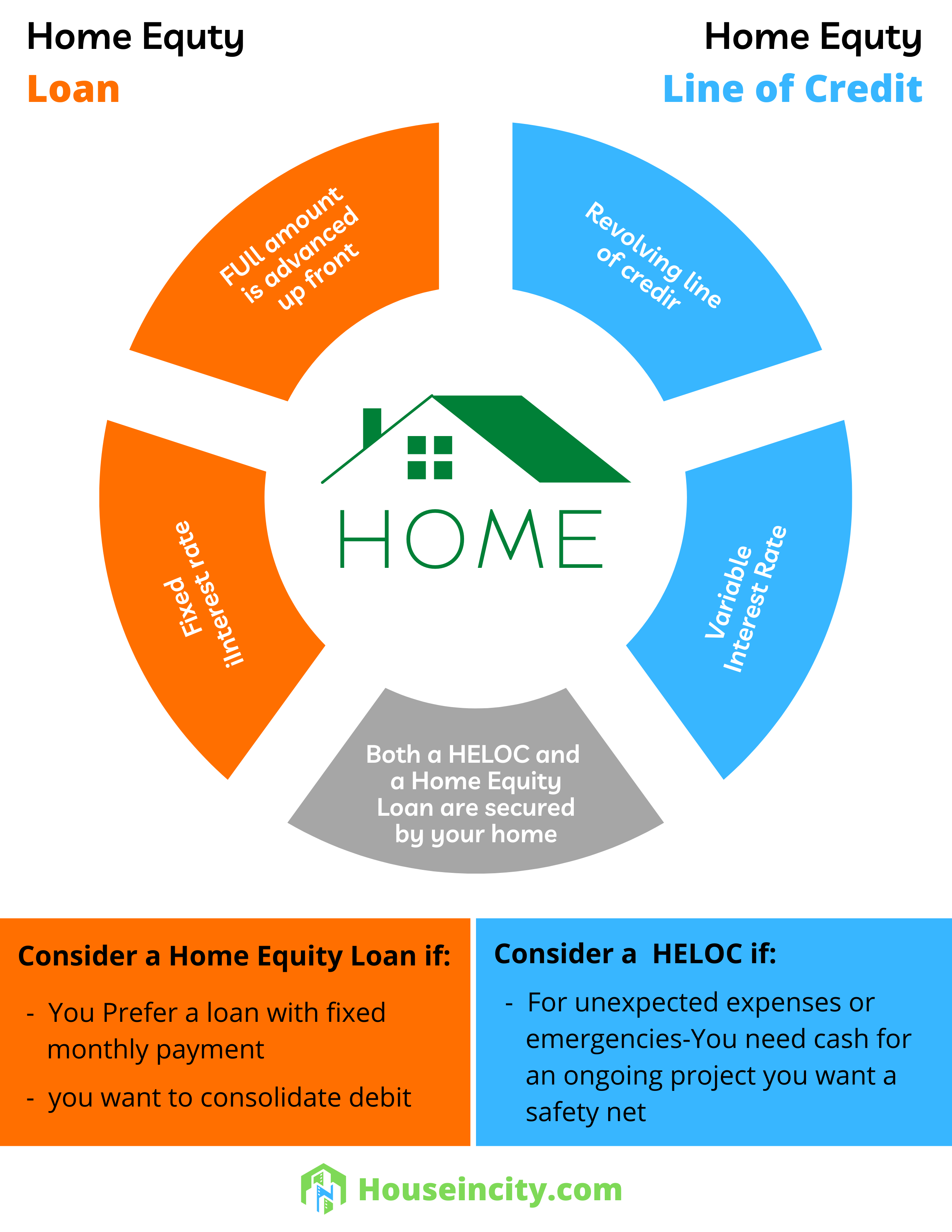

Home Equity Loan vs. Line of Credit

If your home is worth more than your mortgage, you might be wondering how to leverage your equity. Underwater mortgages can make it hard to sell your house and move to a new one. Equity can be hard to come by, but there are a few different options to borrow against your home.

The two options are a home equity loan or a line of credit. A mortgage with a home equity loan is a loan that you take out against your home. You must be able to afford the payments for the loan and the interest, but you have a fixed monthly payment.

Home equity loans are great for consolidating high-interest debt or if you need to make a large purchase. A line of credit is best for “rolling over” unused funds and paying interest on the amount of your borrowed money. A line of credit is a type of loan that allows you to borrow up to a specified limit. You can borrow as much or as little as you need, whenever you need it. You can also borrow more than the limit. You will be charged interest on the money you borrow and charge interest when you use the money. You can borrow and pay interest, then borrow and pay interest again.

A line of credit is a type of loan that can be borrowed anytime you need money, instead of a home equity loan, which is borrowed all at once.

Types of Home Equity Loans

You might have seen that there are many different types of home equity loans. They can be classified into two main groups: fixed-rate and variable-rate.

A fixed-rate home equity loan

A fixed-rate home equity loan is a loan with a fixed interest rate and a fixed monthly payment taken out against the equity (the difference between the home’s current market value and the outstanding mortgage balance) of a home. The borrower can usually choose the loan length, anywhere from five to thirty years. A fixed-rate loan is usually the best option for people who expect to stay in the same home for a long time. A fixed-rate loan is also a good option for people who don’t want to deal with the hassle of refinancing their mortgage.

Advantages of a fixed-rate home equity loan

There are many advantages to a fixed-rate home equity loan. For example, you may be able to access the equity in your home in a low-interest-rate environment. You may also be able to pay the loan off quicker than a variable-rate home equity loan.

Disadvantages of a fixed-rate home equity loan

In a fixed-rate home equity loan, the interest rate does not change for the entire duration of the loan. If the interest rates on your loan are higher than the current market rates, you will not be able to renegotiate your loan. Additionally, the interest rate on a fixed-rate home equity loan often changes after the first few years. This will affect the amount of interest you need to pay back throughout the loan.

Variable-rate home equity loans

Variable-rate home equity loans have become a popular choice for recent college graduates and seniors looking to finance their retirement. This loan is a good choice for those who have a variable interest rate mortgage because they would be able to restructure their mortgage debt.

A variable-rate home equity loan is a good choice for those who have a variable interest rate mortgage because they would be able to restructure their mortgage debt.

Advantages of a variable-rate home equity loans

Everyone needs a little help from time to time, and a variable rate home equity loan can provide a safe and reliable way to get your finances back on track. As your financial obligations change, a variable rate home equity loan can be customized to meet your family’s current needs.

A variable-rate home equity loan is a flexible and easy-to-understand type of funding that can provide a wealth of benefits for homeowners. If you struggle with managing their finances, a variable rate home equity loan might be the answer you need.

Disadvantages of a variable-rate home equity loan

The variable-rate home equity loans are a good option for borrowers who want to use their equity to borrow against their home equity. However, these loans come with higher interest rates and fees, which would increase the amount of money you would have to pay back in the end.

The main difference between these two types of loans is that the interest rate on a fixed-rate loan remains constant for the loan duration. In contrast, the interest rate on a variable-rate loan fluctuates based on prevailing interest rates. Depending on the type of loan you are looking for, the advantages and disadvantages of each type will vary.

What are the requirements to qualify for a home equity loan?

Like any other type of loan, not everyone meets the criteria to access home equity loans. There are many different requirements to qualify for a home equity loan. They include:

- High credit score

Many people are unaware that your credit score is an essential factor in determining whether you will get approved for a home equity loan. A high credit score means you are a trustworthy borrower, and lenders will be more likely to give you a loan. However, if you have a low credit score, it may be more difficult for you to qualify for a home equity loan, and you will have to find alternative options.

As a home equity loan can be an excellent way to consolidate your debts, you must make sure that you are prepared before you apply. A high credit score will help you get approved for a home equity loan, but if you have a low credit score, you may need to consider other options.

- A job or a high income

You may be thinking to yourself, “I don’t need a job to be able to qualify for a home equity loan,” but you’ll be surprised to find out that you’re wrong. To qualify for a home equity loan, you need to have a job or a high income. While some people can get approved for a loan with a low salary, others are not so fortunate. The main reason for this is that the bank needs a backup plan if you lose your job or move. They don’t have to worry about getting the house back if there is a default on the loan.

If you consider a home equity loan, you will need to have a job or a high income to qualify. This is because lenders need to know that you can repay the loan. When you need a loan, you want to make sure you can repay it.

What are the benefits of home equity loans to the consumers?

Home equity loans are one of the main tools to help homeowners take care of their property. Homeowners can take out a loan and use the money to pay for property repairs, home improvements, and other expenditures. Home equity loans can also be used to pay for a college education, take care of healthcare, or just about anything else. Some of the benefits enjoyed by the consumers include:

- Low-interest rates

Many people take out home equity loans because they offer low-interest rates as compared to other forms of debt. If you are struggling to pay off your high-interest credit cards, then a home equity loan may be a more affordable option for you. A home equity loan comes with a fixed interest rate and a monthly payment.

- Easy to obtain

Home equity loans are easy to obtain as compared to other forms of debt. This is because the equity in your home backs them. The more equity you have, the more money you can borrow. Home equity loans allow you to borrow against your home’s value without selling it.

- Tax benefits

Home equity loans provide a way to borrow against your home’s equity to get cash. You used to have to use your 401K or other retirement funds to get cash, but a home equity loan is also an option. The home equity loan may be forgiven if you meet certain conditions. It is essential to consult a tax advisor to determine your specific tax situation before taking a home equity loan.

- Better than refinancing

Home equity loans are much better than refinancing for several reasons:

- You are not putting your home at risk with a home equity loan. If you are refinancing, you are likely to be refinancing a mortgage where the property is at risk.

- A home equity loan is much more affordable than refinancing because the interest rates are typically much lower than refinancing.

- A home equity loan is a good option if you cannot afford the closing costs associated with refinancing.

What are the benefits of home equity loans to the lenders?

For lenders, home equity loans can provide a stable source of income and a way to invest in a low-risk asset.

What is the right way to use a home equity loan?

A home equity loan is a loan that a homeowner can use to pay for anything from home improvements to college tuition. This type of loan is specifically for homeowners but is available to individuals with homes and not just homes with a mortgage.

Are there risks involved with getting a home equity loan?

The recent economic downturn has left many people looking for new ways to improve their financial situation. One way to do this could be by getting a home equity loan. Is there any risk involved with this action?

Whether or not it is risky to get a home equity loan depends on the individual and their situation. From an outside perspective, it seems risky. However, if someone has had a good credit history, steady employment, and reasonable down payment, it might not be a risky decision. This is because the person will have a lower interest rate than someone who does not have those same qualities. Furthermore, the borrower will not have to show the bank any other collateral to get the loan.

In addition to the extremely high-interest rates, you could lose your home if you don’t stay on top of the loan terms.

How to find the right home equity loan

Would you like to know how to find the right home equity loan? The following tips can help:

- Make sure you are fully informed about the interest rates, fees, and repayment terms for the different types of loans.

Loan rates can vary depending on the lender, the type of loan, and the borrower’s credit score. It is essential to be informed about all the specifics and compare rates to get the best rate.

It’s essential to be informed on the interest rates, fees, and repayment terms for the different types of loans. This can help you make the best decision when getting a home equity loan.

- Make sure the loan is in an equity line of credit so funds can be accessed as needed

We all want to get the most for our money, but sometimes we just can’t afford an expensive purchase. So, what do you do? If you have a home, you may want to consider an equity loan. What does an equity loan do for you? First, it may allow you to borrow money for a purchase you otherwise couldn’t afford.

Second, it may allow you to avoid credit cards, which generally have high-interest rates. Third, it may allow you to finance the purchase of a second home and deduct the interest. Lastly, it may allow you to borrow money against your equity, so you can use the funds only when you need them.

- Go with the lender with the best reputation for customer service and who is willing to work with you on repayment plans.

Lenders are the most crucial part of the equation when looking for a home equity loan. Lenders with the best reputation for customer service and who are willing to work with you on repayment plans are the best choice.

Parting Shot

Stepping into something new can be exciting and nerve-wracking. It’s often hard to know the right questions to ask or what to expect. If you are considering a home equity loan, then this article mentions almost everything you need to know. By reading through the blog post, you will find it easy to find the right lender and apply for a loan worth the chase.

Good luck!