When it comes to mortgages, there are many options available to borrowers. One option is to get a loan from Fannie Mae, which is a government-sponsored enterprise (GSE).

What Is Fannie Mae?

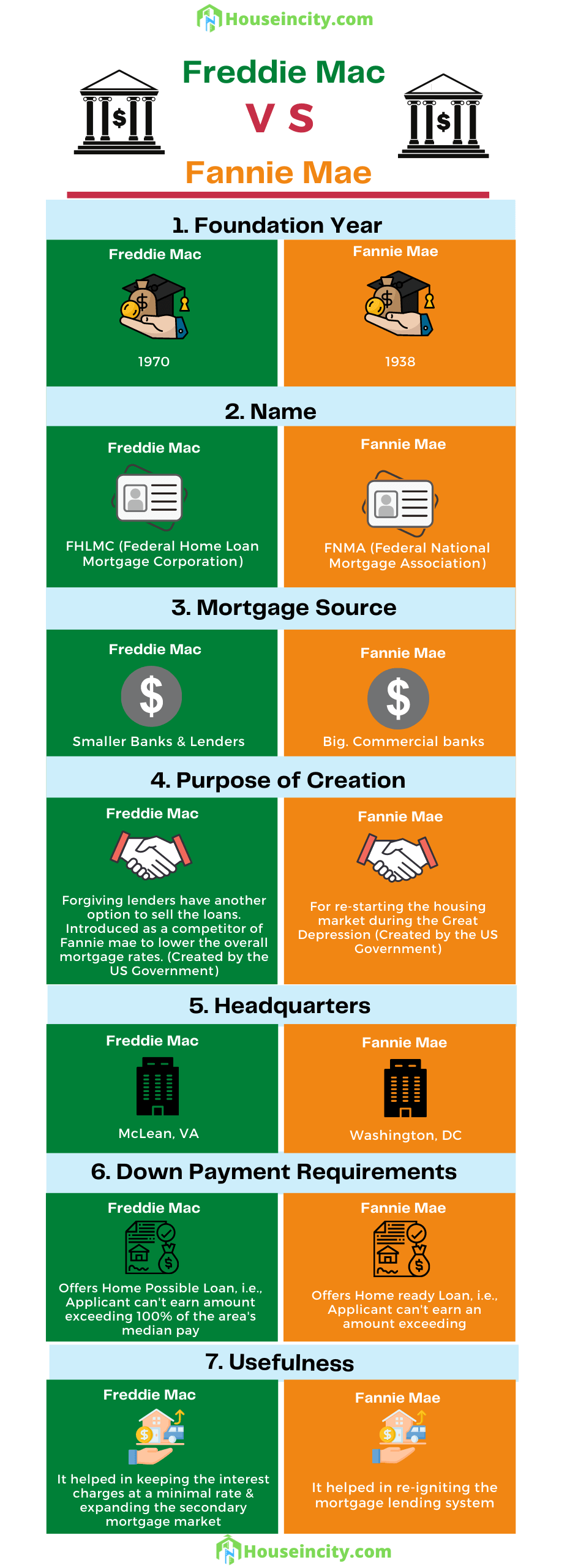

Fannie Mae is a government-sponsored enterprise (GSE) that was created in 1938 to help ensure that there would be a steady flow of mortgage funds available for Americans to buy homes. The organization does this by buying mortgages from lenders and then either holding them in their portfolios or packaging them into securities that are sold to investors.

Fannie Mae is the largest provider of residential mortgage financing in the United States. In 2018, they financed more than $600 billion in single-family loans and nearly $300 billion in multifamily loans.

What are the requirements to qualify for a Fannie Mae loan?

To qualify for a Fannie Mae loan, borrowers must meet certain requirements, including:

- Having a credit score of 620 or higher

- A maximum debt-to-income ratio of 50%

- A minimum down payment of three percent

- Documentation of income and employment history

- A maximum loan amount of $484,350 for a single-family home (higher limits apply in areas with high housing costs)

Fannie Mae Mortgage Programs

There are a few different mortgage programs offered by Fannie Mae, each with its own set of eligibility requirements:

- The HomeReady

This program is designed for low- and moderate-income borrowers, with expanded eligibility for those who are considered underserved. What sets this program apart is that it allows for a down payment as low as three percent (as opposed to the five percent required by most conventional loans) and offers flexible underwriting guidelines. The good thing about having flexible underwriting guidelines is that it allows a broader range of borrowers to qualify.

- The Home Possible

Another program geared towards low- and moderate-income borrowers, this one offers even more flexibility than the HomeReady program. It has no minimum credit score requirement and allows for a down payment as low as three percent.

The key difference between the HomeReady and Home Possible programs is that the latter is available only to first-time homebuyers (or buyers who have not owned a home in the past three years).

- The Conventional 97

As its name would suggest, this program requires just a three percent down payment – making it one of the most accessible loan programs. In addition, there are no income limits or geographic restrictions with this program. The only catch is that you must be a first-time homebuyer (or someone who has not owned a home in the past three years) to qualify.

- RefiNow

Another program offered by Fannie Mae is called RefiNow, which allows borrowers who are current on their mortgage to refinance into a new one without undergoing a whole underwriting process. The main requirements for this program are that you must have a good payment history and enough equity in your home.

- Tenant-In-Place Rental Program

Another program from Fannie Mae worth mentioning is their Tenant-In-Place Rental Program, which allows investors to buy and finance properties with tenants already in place. This can be an excellent option for those looking to invest in a rental property without going through the hassle of finding tenants.

- Mortgage Help Network

This program from Fannie Mae is designed to help borrowers struggling to make their mortgage payments. If you’re having trouble keeping up with your payments, this program can provide you with the resources and assistance you need to get back on track.

One thing to keep in mind is that this program is only available to borrowers who have a Fannie Mae-backed loan.

What Are the Benefits of Getting a Loan from Fannie Mae?

There are several benefits to getting a loan from Fannie Mae:

Lower Interest Rates

You may be able to get a lower interest rate on your loan if Fannie Mae backs it. This is because lenders know that the loan is less likely to default, so they are willing to offer lower rates.

Fixed-Rate Loans

Fannie Mae offers both fixed-rate and adjustable-rate mortgages (ARMs). Fixed-rate loans have an interest rate that remains the same for the life of the loan, while ARMs start with a lower interest rate that can increase or decrease over time.

Lower Down Payment Requirements

If you cannot make a 20% down payment on a home, you may still be able to qualify for a loan with a smaller down payment if Fannie Mae backs it.

A wide variety of mortgage products to choose from

Another benefit of Fannie Mae is that they offer a wide variety of mortgage products. This includes products for low- and moderate-income borrowers and loans for energy-efficient homes.

While Fannie Mae is an excellent option for many homebuyers, it’s not the only option. Be sure to speak with a mortgage loan officer to learn more about your mortgage options.

What Are the Disadvantages of Getting a Loan from Fannie Mae?

While there are some advantages to getting a loan from Fannie Mae, there are also some disadvantages:

Mortgage Insurance Requirements

If you make a down payment of less than 20%, you will be required to pay mortgage insurance. This insurance protects the lender in case you default on the loan.

Limited Loan Options

Fannie Mae only offers specific types of loans, such as fixed-rate and adjustable-rate mortgages. If you are looking for a specific type of loan, such as an interest-only loan, you will not be able to get it through Fannie Mae.

Higher Interest Rates for Some Borrowers

While Fannie Mae generally offers lower interest rates, some borrowers may not qualify for the best rates. This is because Fannie Mae loans are priced based on creditworthiness, and some borrowers may not have a high enough credit score to get the best rate.

Fannie Mae FAQs

What is the difference between Fannie Mae and Freddie Mac?

Fannie Mae and Freddie Mac are both government-sponsored enterprises (GSEs) created to provide stability in the mortgage market. They accomplish this by buying loans from lenders and either holding them in their portfolios or packaging them into mortgage-backed securities (MBSes) and selling them to investors. While they have similar purposes, there are some critical differences between the two:

- Fannie Mae was created in 1938, while Freddie Mac was created in 1970.

- Fannie Mae is a publicly-traded company, while Freddie Mac is a private company.

- Fannie Mae only deals with conforming loans, while Freddie Mac purchases both conforming and non-conforming loans.

What types of loans does Fannie Mae offer?

Fannie Mae offers both fixed-rate and adjustable-rate mortgages (ARMs). Fixed-rate loans have an interest rate that remains the same for the life of the loan, while ARMs start with a lower interest rate that can increase or decrease over time.

How do I know if Fannie Mae backs my loan?

If you are not sure if Fannie Mae backs your loan, you can check their website or give them a call. You will need to provide them with your name, address, and the last four digits of your Social Security number so they can look up your loan information.

What are the requirements for a Fannie Mae loan?

The requirements for a Fannie Mae loan vary depending on the type of loan you are applying for. For example, the down payment requirements are different for fixed-rate loans and adjustable-rate mortgages. You can find all of the specific requirements on their website.

Do I have to pay mortgage insurance if I get a Fannie Mae loan?

If you make a down payment of less than 20%, you will be required to pay mortgage insurance. This insurance protects the lender in case you default on the loan.

Is it better to get a loan from Fannie Mae or a bank?

The answer to this question depends on your individual circumstances. You will need to compare the terms of the loans that you are eligible for to decide which one is right for you. You may want to consider the interest rate, down payment requirements, and whether or not you will have to pay mortgage insurance.

Speak with a loan officer at a bank and compare your options before deciding.

Do I have to use a specific lender if I want a Fannie Mae loan?

No, you are not required to use a specific lender. You can shop around and compare rates from different lenders before choosing one.

What is the minimum credit score for a Fannie Mae loan?

The minimum credit score for a Fannie Mae loan is 620. However, borrowers with a credit score of 700 or higher will generally get better interest rates.

What is the maximum debt-to-income ratio for a Fannie Mae loan?

The maximum debt-to-income ratio for a Fannie Mae loan is 45%. Your monthly debts (including your mortgage payment) should not be more than 45% of your monthly income.

What is the minimum down payment for a Fannie Mae loan?

The minimum down payment for a Fannie Mae loan is generally between five and ten percent. However, this amount can vary depending on the type of loan you are applying for.

What are the fees associated with a Fannie Mae loan?

The fees associated with a Fannie Mae loan depend on the type of loan you are applying for. For example, there may be origination fees, appraisal fees, or application fees. You can find more information about specific fees on their website.

Do your research and compare the fees charged by different lenders before choosing one.

Is it hard to qualify for a Fannie Mae loan?

The answer to this question depends on your individual circumstances. The requirements for a Fannie Mae loan vary depending on the type of loan you are applying for. You can find all of the specific requirements on their website.

Speak with a loan officer to know whether or not you will qualify for a particular loan before you apply.

What is the interest rate for a Fannie Mae loan?

The interest rate for a Fannie Mae loan depends on the type of loan you are applying for, your credit score, and other factors. You can use their online calculator to estimate what your interest rate might be.

Final Word

As you can see, there is a lot to know about Fannie Mae loans. However, doing your research and speaking with a loan officer will help you determine if this type of loan is right for you.