If you need a loan, getting one for the first time can be a difficult experience. Before you take one, you’ll need to save hundreds of dollars for property taxes, closing costs, and a down payment. You’ll have to show your lender a good credit history in addition to dealing with a lot of paperwork.

As such there are different types of loans that individuals can take. If you’re planning to get a mortgage loan, there’s one thing you needn’t stress about. That’s knowing the exact amount you will have to pay for your mortgage on a monthly basis. This is made possible using the amortization schedule, a table that details the number of monthly mortgage payments you have to make and the amount of money you have to pay to the lender each time.

Lenders also use this amortization table to figure out the borrowers’ monthly payments and loan repayment details. By going through your mortgage amortization schedule, you won’t end up being surprised while making monthly payments. Let’s find out everything you need to know about the loan amortization schedule to gain a better insight.

What is Amortization?

In real estate, amortization is the process of repaying mortgage loans using regular monthly payments. When you’re taking an amortization schedule for mortgage, a flat monthly payment will be specified on the loan terms. Throughout the duration of the loan period, the monthly payment is applicable for both the principal amount and interest due on the loan.

For instance, if you have taken a fixed-rate mortgage for 30 years, you’ll have to make fixed monthly payments referred to as amortization. By making these payments without default for 30 years, you will be able to pay off the loan. The monthly payments of a fixed-rate loan stays relatively constant, as the interest rates of these loans do not change. The payments may increase or dip slightly based on your insurance costs or property taxes fluctuations.

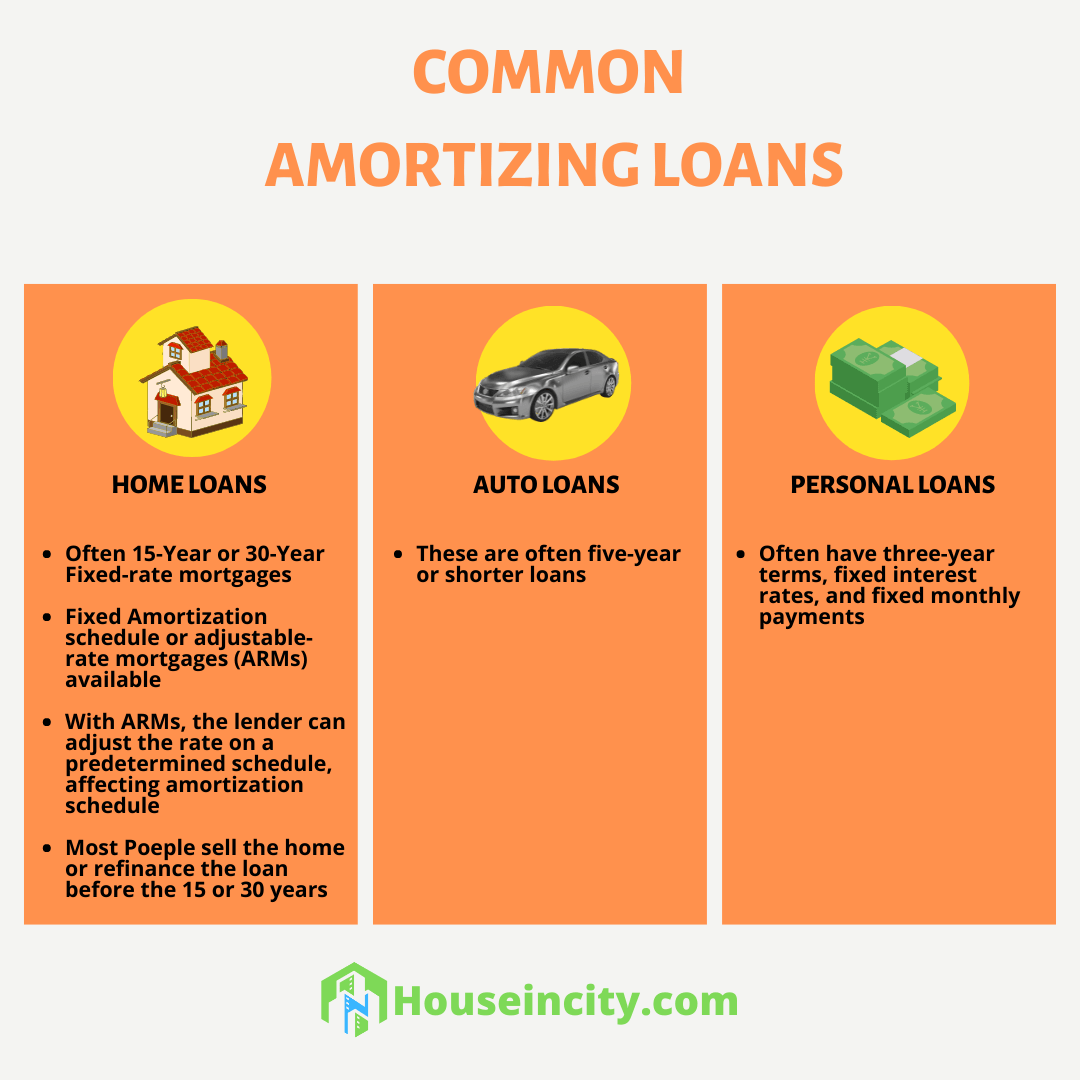

Types of Amortizing Loans

Beyond mortgage amortization loans, you’ll come across different amortized loans that vary based on repayment schedules and payment amounts based on the loan term and interest rates set by the lender. Some of the common amortized loans are:

- Auto loans.

- Personal loans.

- Student loans.

- Fixed rate mortgages.

- Home equity loans.

When it comes to mortgage and auto loans, most of the initial payments go towards repaying the loan interest. A high percentage of the monthly payment pays off the loan’s principal amount on each subsequent payment. This is why you need an amortization chart to figure out how much of the monthly loan payment goes to paying off the interest and principal amount. The amortization mortgage schedule also clearly depicts how much amount you need to part with on a monthly basis during the full payment schedule.

What Is A Mortgage Amortization Schedule?

An amortization schedule, also known as amortization table, is the list that details out the monthly payments of an amortized loan over time. The table depicts how much you need to pay as monthly payments, how much will go for paying off the loan’s interest and principal amount.

Initially, while paying off the amortized mortgage loan, the amortization schedule indicates that most of the payment is used to pay off the interest. After making payments for several years, this trend shifts, where most of the payments go towards paying off your loan’s principal balance. With the help of an amortization schedule mortgage table, you will be able to view the beginning balance of your monthly mortgage payment and the remaining balance once you made the payment.

As for the basic amortization schedule with fixed monthly payment details does not list any extra payments. But this doesn’t mean you can’t pay an extra amount to pay off the loan quickly. Furthermore, additional fees or costs incurred while paying off loans do not make it to the amortization schedule. In general, the amortization schedule lists out only the scheduled payments for fixed-rate loans and not variable rate loans, lines of credit, or adjustable-rate mortgage loans.

Understanding the Amortization Schedule

Based on your specific loan, you can create your own loan amortization schedule using any mortgage calculator to figure out the total mortgage costs you will incur while taking out the loan. Based on your personal circumstances and the loan amount, the amortization table can be customized to suit your preferences.

The amount of interest charged for each monthly payment varies based on the outstanding balance of the loan and the initially specified interest rate. You can repay the principal amount with the remaining part of the periodic payment. The portion of principal repayment is what reduces the outstanding loan balance.

With the help of sophisticated amortization schedule calculators, you can compare how accelerating the payments helps in repaying the loans quickly. For instance, if you’re expecting to receive a yearly bonus or inheritance, you can include this in your schedule and see how it affects the interest charges and the loan’s maturity date over the loan term. This is applicable for student loans, auto loans, personal loans, mortgage loans, or other fixed term loans.

Each of these loans is given a fixed term in advance and a fixed interest-rate that sets the monthly loan repayment amount. But, the loan terms vary based on the type of asset.

Some common ones are:

| Loan Types | Loan Term |

| Mortgage Loans | 15 to 30 years. |

| Auto loans | Upto five years. |

| Personal Loans | Three years. |

How Do Amortization Schedules Work?

As for the loan amortization schedule breaks down the loan balance into equal repayment amounts depending on the fixed-rate loan amount, interest-rate, and loan term. This schedule also enables the borrowers to see the amount they will have to pay each month and the outstanding balance after each payment.

In an amortization schedule, the percentage of monthly payment that goes towards paying the principal balance increases after each payment, and the percentage used for paying the interest decreases after each payment. Based on the type of loan you have taken, the principal or interest payment percentage varies. Using the loan amortization formula, you can calculate how much you will have to pay each month as principal repayment and interest charges depending on the loan term and total loan amount.

How to Make an Amortization Table?

By understanding the amortization table definition and the breakup details you can build your loan repayments table. The easiest way to amortize a loan is to create a template where the relevant calculations are automated. An amortization schedule based on payment includes the following:

- Details of the loan: For loan amortization calculations, the amount varies based on the specific loan amount, interest rate, and loan term. There is a space allocated to enter this information for those who are using an online amortization table or calculator.

- Total monthly loan payment: Using the amortization schedule template, the total loan payment will be automatically calculated. You can also calculate it manually or with the help of a personal loan calculator.

- Loan Payment frequency: In the amortization table, the payment frequency indicates how often you will have to make the payment. In most cases, the monthly loan payment is the common payment option.

- Principal balance payment: This amount in the amortization schedule shows how much of the monthly payment is used for paying the loan‘s principal amount. During the life of the loan term, the percentage of this amount keeps increasing after each monthly payment for amortized loans.

- Interest charges: Similar to the principal payment, the interest costs in the amortization schedule indicate how much of the monthly payment goes to paying off the loan’s interest. With each monthly payment, the percentage of interest payments decreases over time.

- Outstanding balance: The outstanding balance is the amount of the loan that remains after making the scheduled monthly payments.

- Additional payments: If you make additional payments beyond the stipulated monthly loan payments, the amortization schedule will use the extra amount to pay off the principal balance. The future interest costs will be calculated based on the updated balance after the payment.

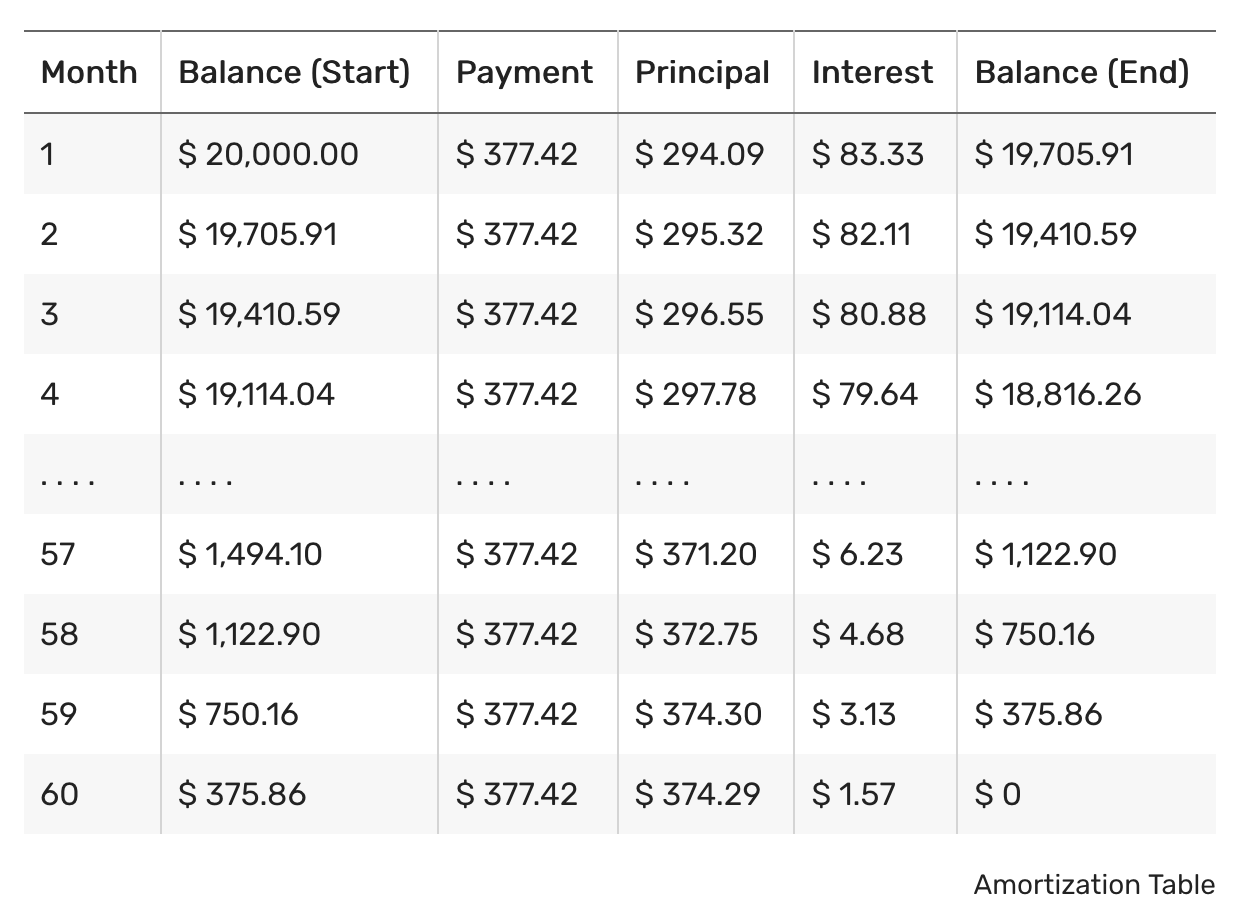

Amortization Table Example

Final Word

Having a clear understanding of the loan amortization schedule of the loan you’re planning to take or the loan you already have will help you get a bigger picture about the amount you will have to set aside for repaying the loan. By simply comparing the amortization schedules using different options or an amortization schedule example, you would be able to decide how much total loan cost you’ll have to pay, which loan terms are apt for your financial situation, and whether you should take a loan or not.

When the lender gives you the loan amortization schedule, it’s quite normal to ignore it and the piles of paperwork you will have to deal with. But, going through the details listed out on the amortization schedule plays a crucial role in giving you a better understanding of the ins and outs of the specific loan. For instance, if you have to pay off debts, checking the information on the loan amortization schedule about your existing loan will help you figure out where you need to focus on your payments. Also, by understanding how the amortization schedule is calculated, you will be able to figure out how to pay off your loans quickly.