So, now that you have found your dream house! Before buying it, you should ask yourself, ‘how much house can I afford?’

Buying a new home is exciting, but it is also a huge undertaking. A house should give the owner a sense of stability and financial security. It needs to help you make sensible decisions and be realistic about, “what kind of house can I afford?” Otherwise, you would be left with brooding and thinking, “I could find myself living month to month with just enough money to meet all my needs, mortgage payments, utilities, grocery, or other debt payments.” To not buy a house that you cannot afford, you need to understand and plan your housing budget.

First, you should find out about the amount of mortgage you will qualify for, and this will depend on how much debt lenders agree to offer. A lender will decide this after evaluating how much you can take on. This will give you the answer to “how much mortgage can I afford?”

Can you afford the house?

Calculating how much house you can afford before making any decision is the most prudent thing to do. Your monthly income and monthly expenses, including debts such as car and student loans, will all have to be accounted for to the amount you can afford. As a home buyer, you will find a lot of comfort after understanding & calculating your monthly mortgage payments. You want to look for homes that are in your price range. Knowing your budget and then sticking to it will make buying a house a very smooth process.

Usually, the monthly household incomes and debts remain stable, but unexpected expenses can impact your savings. It is considered good financial planning to have a three-month reserve of payments, including your housing payments and monthly debts. This cushion can keep you going even when there are unexpected expenses.

Calculating home affordability

There are plenty of home affordability calculators available online that allows you to find out and answers your question, ‘what house can I afford?’ and “how much cash you need for the down payment?” The calculator will ask for your yearly income, monthly debts, and savings for the down payment. The calculator will let you know how big a loan you can take and answer the question, “how much home can I afford?” If you already have a price in mind, then the how much house can I afford calculator will help you find out the cash you need for the down payment and closing costs.

What is the 29/41 rule, and how does it help calculate home affordability?

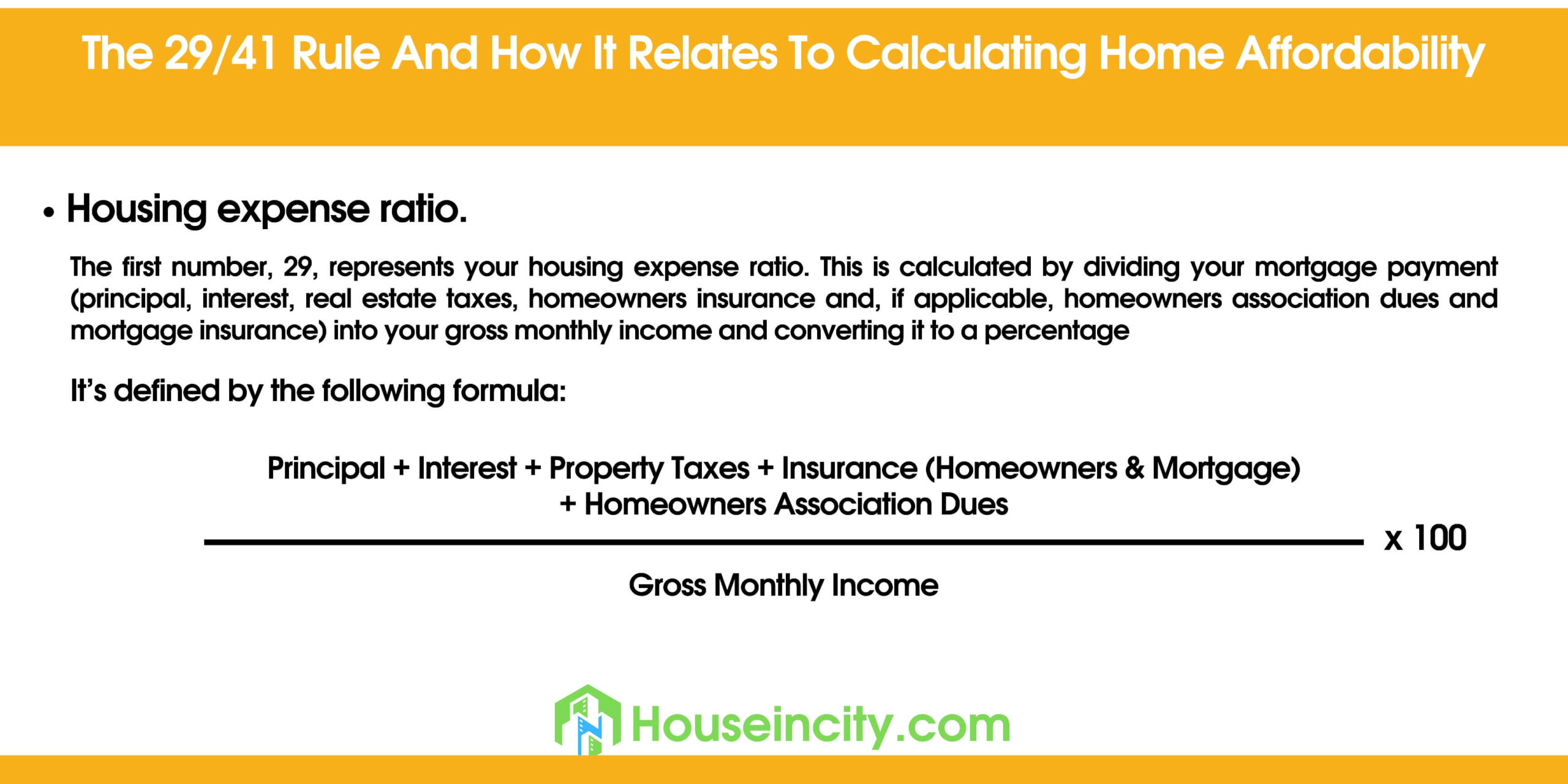

Lenders will calculate your debt-to-income (DTI) ratio while evaluating your mortgage application. Do read on, this ratio is explained in detail in the article, and it will give you an understanding of the basic premise here. This ratio is calculated by dividing the monthly debt payments by total monthly income. How much house can I afford rule of thumb says that following the 29/41 rule is ideal?

The first number, 29, is for the housing expense ratio. It is calculated by dividing your complete mortgage payment, including principal amount, interest, real estate tax, insurance, and other expenses due, by gross monthly income. Then it is multiplied by a hundred to turn it into a percentage. Look at the following formula:

Principal +Interest +Insurance + Property Tax + other dues as homeowners

Divided by Gross monthly income and then multiplied by 100.

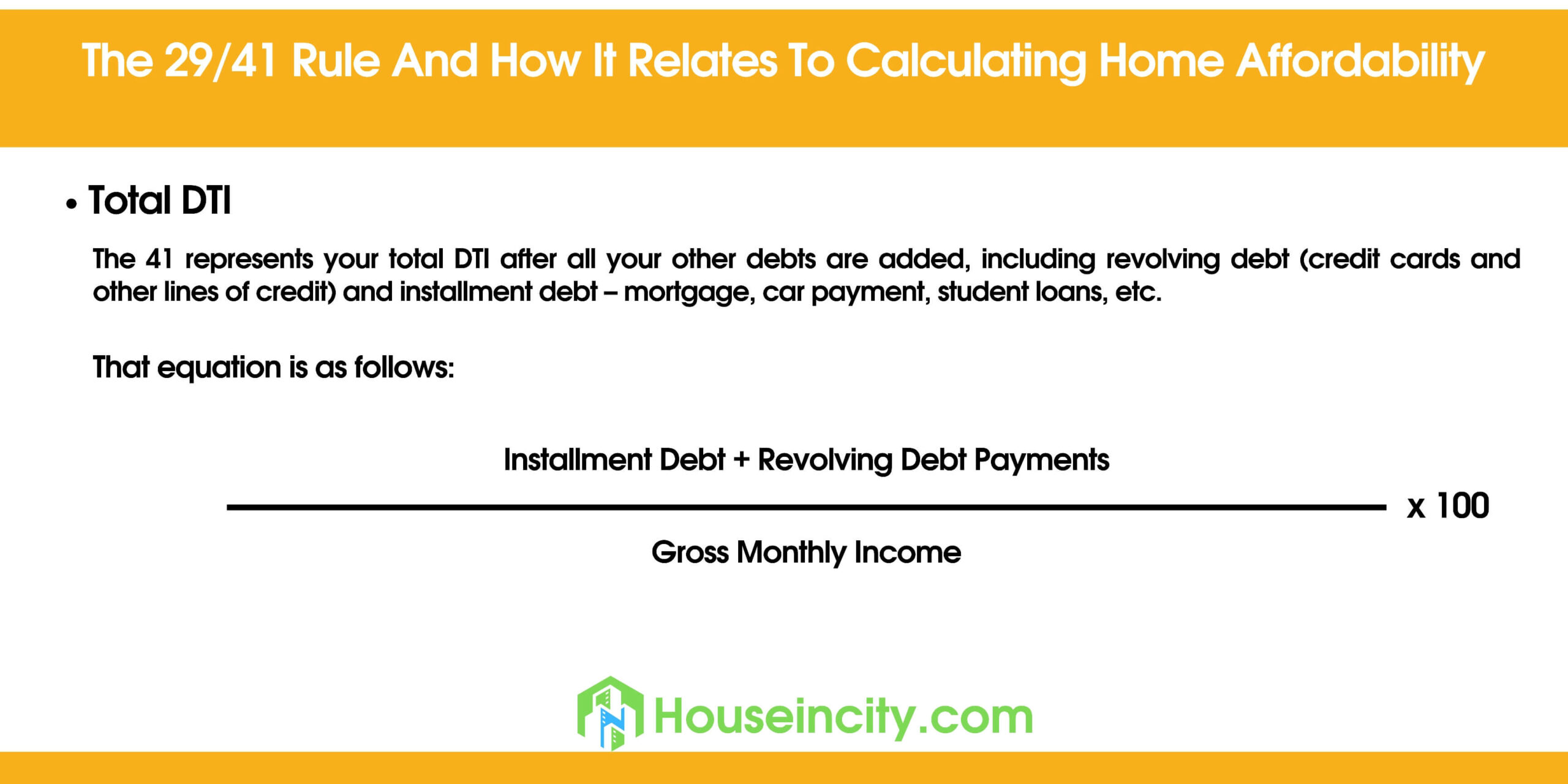

The next number is 41. It represents the total DTI. The formula for this is somewhat like this:

Installments amounts + monthly debt payments

Divided by gross monthly income and then multiplied by 100

The 29/41 rule is a good starting point, but there can be exceptions. It is good to know this before finding out about mortgage qualifications. Lenders use DTI to determine your ability to pay back. According to this rule, your mortgage payments should not be more than 29%, and the total monthly debts should not be more than 41% of your total monthly income.

DTI ratio and its impact on mortgage affordability

A lender such as a bank will look at the DTI (Debt To Income) ratio to find out how much money they can lend you, and it will also give you an idea if you are wondering, “how much can I afford for a house?” They will stack your monthly debts and compare them with your monthly income. Usually, housing expenses should be between 28% and 36% of the monthly income. The higher range is for people with high credit scores and clean credit history.

Let us look at this example:

If your monthly mortgage payment with insurance and taxes is $1400 per month and your monthly income is $5000 before taxes, then.

1400 divided by 5000 = 0.28

This means your DTI is 28 %. It is best if you keep the DTI in this range; otherwise, the mortgage payments can become a burden on you.

Calculating your DTI ratio

It is a simple ratio, yet lenders place a lot of importance on this ratio and use it as a qualifying factor. Before approving any loan, the lenders want to know the amount of debt you have and treat that as an indicator of your repayment capability. So, here is how DTI is calculated:

- Add all your monthly debts

- House payments or monthly rent

- Student and car loan

- Child support or alimony

- Credit card payments

- Any other debts

You can exclude your grocery & utility bills and other bills that vary from month to month.

- Add up your monthly gross income from your job, rent, or other sources.

- Now divide the monthly debts by the monthly income.

For example:

If your debts are $1600 every month and your monthly income before tax is $5000, the DTI ratio is 0.32 or 32%.

Is it possible to improve the DTI ratio?

Are you wondering, “How much mortgage can I qualify for?” If you are keen on buying a house but have too much debt, you will fail to get a mortgage on good terms. You can try to improve your Debt To Income ratio. Here are the three ways you can do this:

- Debt consolidation

- Paying off your existing debt

- Increase your income by some means

All of these steps will take some time, and you should remain aware and ready for any opportunities that come your way. Lowering DTI is possible but not very easy. If you manage to do it, you will have a better chance of getting a favorable mortgage.

Which other factors affect your house affordability?

Yes, the DTI ratio is important, so it is important to know, “how much mortgage can I get approved for?” at this stage. This depends on other factors such as:

- Term of the mortgage refers to the length of time you have to pay back the mortgage. Usually, the mortgage terms are between 15 and 30 years. There are other terms also available based on various factors. The mortgage terms impact your monthly payments. How much mortgage can you afford?

Here is an example:

If you buy a house worth $250,000 at a fixed rate of the mortgage at 4% for 15 years, then your monthly payment will be approximately $2222. 25.

However, if you change the length of the period to 30 years but leave the cost of the house and the interest rate the same, you will have to pay $1527.77.

The monthly mortgage payments will probably be the biggest debt you need to pay off. It is extremely important to understand and make sure that you can afford it.

- The interest rate on the mortgage: your lender will set the interest rate on your mortgage, and it can be either fixed or adjustable. The rates may remain the same or change accordingly. The interest rate charged will depend on various factors, including your credit score and history, amount of down payment, etc. Even a small change in the interest rate can affect you heavily. If you look at the same example and plan to buy the same $ 250,000 house at 4.5 % for 15 years, instead of 4%, your monthly payment would go up to $2326.37. A small change in the rate of interest can end up in you paying hundreds or thousands of dollars extra.

- Monthly budget: after calculating your DTI and all the debts you have, the next thing you need to think about is your monthly budget. A budget will help you plan and make place for the monthly mortgage payment. If you don’t have a budget, you can create one easily by keeping tabs on your expenditure and income for a couple of months. Several budget apps available online can help you in your financial planning. There are two main reasons why anyone needs to look at their savings, assets, and budget. It is only after this that you can find the answer to the question, “how much home can I qualify for?”

- You ought to know so that you use the savings for a down payment

- The second reason is something called reserves. Reserves are the number of mortgage payments that you can make even if you lost your job or some other event impacted your payment ability. Every mortgage comes with different terms, but it is good to keep at least 2- or 3-months’ worth of payments in the savings account.

When you start tracking your income and expenditure, you may find that either you are left with some extra money and so can afford a higher mortgage, or on the other hand, if you are left with less money, you may rethink the mortgage terms and bring the monthly payment down.

- Down payment: there doesn’t need to be a fixed down payment amount like 20 % or 25% for a mortgage. It is possible to get a mortgage with as low as a 5% down payment. There are some clear advantages of a higher down payment and cannot be ignored.

- Interest rates are mainly decided according to down payment and average FICO score. The higher you make the down payment, the better interest rates you will get. Lenders are happier with higher down payments and find such customers less risky.

- With a lower down payment, you may have to pay for mortgage insurance, which can be equal to a month’s payment, and even an upfront fee, depending on the amount of the mortgage. The mortgage insurance is a protection for the lenders.

It is important to see down payments as an important factor in calculating mortgage affordability.

- Extra costs: apart from the down payment and mortgage insurance, you also need to consider the homeowner’s insurance, closing cost, and taxes.

- Homeowner’s insurance: the homeowner’s insurance will depend on the location, the neighborhood, and the house you buy. The calculation for insurance will look at the value of the property and the value of your at-risk assets. A professional insurance agent will be able to give you an idea about your future homeowner’s insurance amount.

- Closing costs: the last step in buying a house is paying the closing cost. The lender will estimate the closing cost by adding the appraisal fee, title search fee, credit report charges, and more. Usually, the closing cost can be between 3% to 6%.

- Taxes: anyone who owns a property has to pay property tax. This is calculated as per the property’s assessed value multiplied by the local tax rate.

Some tips for buying an affordable house

So, you have found your dream house, and you are ready to buy it. Luckily, you have found a lender who agrees to give you a huge home loan. Does this mean that you go ahead and borrow the whole amount? Do you realize that a huge loan can put you under tremendous financial strain? You need to ask yourself, ‘how expensive of a house can I afford?’

Understand the full implications of taking a huge mortgage and assess your financial situation carefully.

If there is any change in your professional situation, you need to ask, ‘what mortgage can I afford?’ Lenders check the work history and credit score before they say yes. However, if you take a big mortgage, it will be difficult to make the payments during periods of unemployment.

You must know, “the type of mortgage loan I apply for” and “how much mortgage do I qualify for?” are two different things. Each of the following loans will lead you down a different financial path:

- Conventional loans: with a conventional loan, you may get a house with a low down payment of just about 3%. They also have lower interest rates.

- VA loan: this option is available to veterans and service members of the USA. Though traditional lenders offer these loans, they are backed by the US Department of Veteran Affairs. There is no requirement for a down payment for these loans.

- FHA loan: this loan is backed by the Federal Housing Administration. People with lower credit scores and less money for a down payment may qualify for this loan. So, it is better to ask yourself, how much house can I afford fha vs VA.

- USDA loan: this loan is backed by the US Department of Agriculture. People who want to buy property in a rural or suburban area can qualify for this loan. You can also get a USDA loan without any down payment if you are in the low-income bracket.

- Jumbo loan: as the name suggests, these loans are for amounts higher than the current conforming loan limit. You will need to make a bigger down payment and must also have a high credit score to be eligible for this loan.

Unexpected expenditures and emergencies can spoil all your financial plans. Costly medical treatments, damage due to weather, or even an unplanned but necessary trip can spell financial disaster. Ask yourself if it is good to put all your money towards paying the mortgage? Saving for a rainy day and having a safety cushion is important.

Consider buying for much less money than you can afford. This way, you are left with the option to bid if there is a competition or if you get the house, then you will have the money to renovate and design it with the saved money. Not putting all your money into buying the house is a good decision.

If you will be uncomfortable paying the mortgage and don’t have much savings, then why don’t you wait for some time before buying a house? Maybe if you wait and save some money, you will be in a better position. You can pay more as a down payment and get better mortgage terms too.

Final thoughts

Buying a house requires a lot of time, effort, and money. It is an emotional decision for many first-time home buyers. It is extremely important to make decisions fully aware of your financial position. Ask yourself, ‘what price house can I afford?’

After all, how much house you can afford will depend on your financial situation?

House buying decisions should be based on real data and not just on likings or preferences. Evaluating your financial position with clarity will give you a clear picture of your capabilities and ability to pay back the mortgage.

- Start researching as soon as you decide to buy a home. Learn as much as you can about different mortgage options.

- After checking your finances, find out how much house can you afford

- Get pre-qualified and pre-approved for loans so that you know much mortgage you get

- Find the right lender with the right terms

- Look for a house in your budget, and then go for it

With the right planning and enough information, you will be able to buy your dream house in no time.