In today’s article, we would talk about APR, what is APR, its definition, its guide, its explanation, and how it benefits and affects your investment portfolio. To get a better idea of the APR, we would suggest that you do complete thorough research on this matter and therefore proceed to read our article here completely. If you have done a lot of investments in your portfolio, then you might have already familiarized yourself with APR.

So, what is exactly APR? APR is short for the Annual Percentage Rate. It generally refers to the yearly income or interest, generated through the total sums charged to borrowers, or it can also be what is paid to the investors.

What Is the APR Rate?

To put it simply, APR is a percentage that represents the yearly cost of funds over the loan, or the yearly income that has been earned on a certain investment. When borrowing money, for example, APR is the yearly interest that you should pay annually when you are proposing a credit/loan, and when you are lending the loan, and then it is the percentage of interest rate that will be paid to you annually aside from the credit itself.

In essence, the APR is the interest rate that is applied to the loan/credits you have borrowed. This loan ranges from bank loans, vehicle credit, home mortgage loans, students loan, and many other loans. APR will show the total interest rate that you will need to pay when you are proposing a loan from the lender.

Same for vice versa, the APR was the total interest rate that has been accepted from both parties (the lender and loaner), and the total interest rate will be paid yearly, alongside the total paid loan.

The lower the APR, the lower rate that you need to pay for the interest rate when you are paying your debt, and the opposite are also true, the higher the APR rate, the more you would need to pay when you are paying your debt.

What Is The Difference Between Apr and The Interest Rate?

How does APR work? Is it the same as loan percentage rare? If it is the same, why don’t we call it year loan interest percentage rate then? So how does it work? APR is the total interest rate that you would need to pay if you are proposing a loan, the lower the APR, the lower the total interest rate you would need to pay in one year.

However, the APR itself also includes another rate, not just the annual interest rate, such as insurance fee, loan fee, mortgage fee, administration fee, and so on.

According to the National Consumer Financial Protection Bureau, the APR includes a more detailed and wider rate compared with the general interest rate. So, how APR is calculated, it was the total amount of the interest rate yearly, plus another financial fee, for example, the administration fee, and insurance fee, then the rate will be accepted by every party before the loan can be given.

The APR calculation includes the interest rate that was accepted by both parties and another fee from the loan fees, administration, insurance, and so on. Even though the APR itself was considered a wider and more detailed calculation than the interest rate alone, in some countries, the credit interest itself was the APR, so there is no distinction between them.

Notable Facts on How Does Apr Interest Work

To help you better understand what is an annual percentage rate, and how it works regarding the annual interest rate loan, here are a few key notable features.

- APR is the total yearly rate charged for a loan, and also earned from the investment – APR represents the total interest rate that you have charged from the loan, and you will need to pay for the total amount of APR annually. The APR is also earned in investment, the amount you get from investment APR depends on the contract agreement.

- Financial institutions must always disclose the financial instruments of the APR before the contract of loan is signed – APR aims to ensure fair trade agreements, and therefore, the financial institutions as the lender would need to always disclose their financial instruments before the loan was signed and given.

- APR will not reflect the actual cost of loans since lenders will have a fair total amount of leeway during the calculations. (Exclude certain fees) – APR itself won’t reflect the cost of loaning, and lenders will have the total amount of leeway during calculations of the APR.

- APR represents the consistent basis that presents a yearly interest rate. This is information that protects the consumer from misinformation in advertisements – APR is aimed to protect the consumer from misinformation and protect it from unfair loans. The total APR needs to be calculated before lending and therefore agreed upon by both parties.

- APR is different from Annual Percentage Yield (APY) – APR is different from APY, as it essentially has two different calculations and purposes.

These notable facts about the APR are the fundamental aspects of the APR that you should know. APR is the yearly amount of interest rate that needs to be paid. During the agreement of the loan, both the parties, lenders, and loaners will agree on the total amount of an APR, if there is an APR. The total amount of APR mostly will include other extra fees, such as the insurance fee and so on.

APR aims to create a safe, and fair loaning system for the loaners, and create more interest rates from the credits for the lenders. These are instructional instruments needed for the fair trade agreement for both parties.

To know more about APR, we would also recommend you know how to calculate APR, and also how to calculate it for a different purpose. Different loans will have different prices, fees, interest, and the total APR that should be paid. You need to know how to calculate APR to know that you will be handed the correct amount of APR and avoid scamming too.

How Does APR Works?

APR is represented by the interest rate for one year, so it is calculated based on the percentage of the principal payment that you’ll pay once a year. However, it also considers monthly payments and the total amount of APR you will receive will also deduct from monthly payments.

APR is an annual interest rate from the loaners/investor that will be paid based on the investment; however, it is calculated without taking into account the compounding interest every year, basically the interest rate that has been owned by the lender to the investor.

The TILA (Truth in Lending Act) is a mandate that has been implemented since 1968, it states that every lender need to disclose the exact amount of APR they put upon borrowers, and the APR is to be calculated in transparent condition, meaning that borrowers would also see and understand how the calculation taking into account. This is to give transparency to lenders, loaners, and the investment environment.

For example, Credit card companies would need to advertise and show their interest rate monthly, showing to all of their customers, and potential customers how they apply the interest rate, and their rates each month. However, before customers sign any contract with credit card companies, the companies will need to create a clear report on the APR, before they can sign a contract.

How to Calculate APR on a Loan

How to figure out APR on a loan? If you are planning on getting a loan, then you would need to understand how you calculate APR, especially if you are planning to get a loan from a financial institute such as a bank, or Credit Card Company.

To calculate APR on a loan, there are many things to know and take into consideration, such as the principal amount of money, how long that loan will last, the number of the years you will need to pay for the loan, extra charges such as insurances, and additional interest if there are any. Follow these steps to know how you calculate APR for a loan.

- First, calculate your interest rate

- Add administrative fees, add it to the interest amount

- Divide the loan by the total amount of principal

- Divide by total numbers for how long the loan terms (how many days)

- Multiply all of it by 365 (for one year)

- Now, multiply it by 100 (convert it into a percentage)

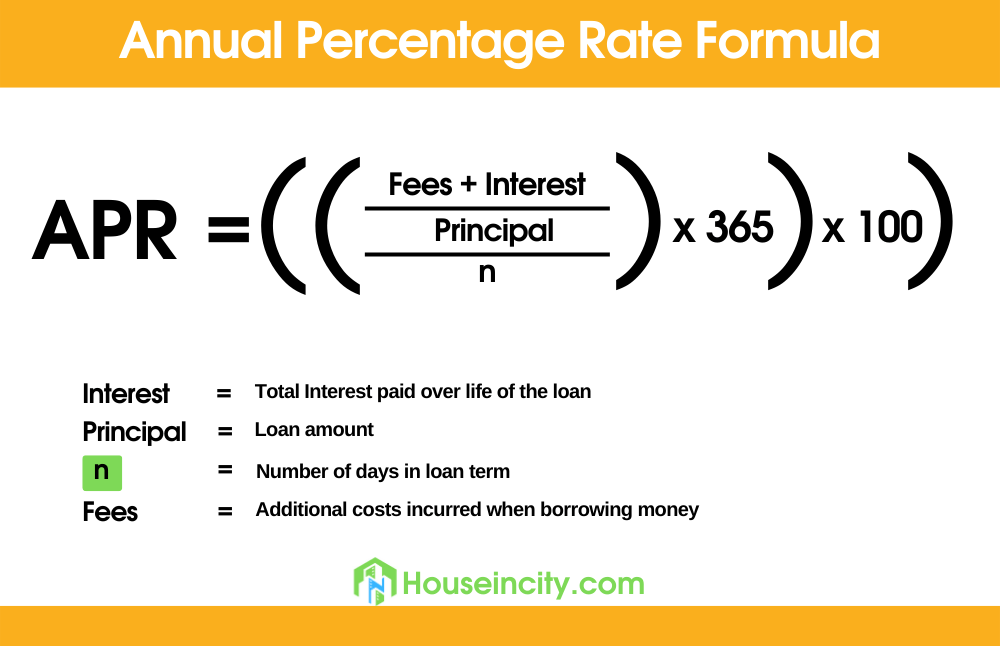

The formula is APR = (Interest + Fee: loan amount): the loan terms, how many days) x 365. Then the percentage of the results.

How to Calculate APR on a Mortgage

To figure out how to calculate APR on the mortgage isn’t so much different from how you calculate it on a loan, or how to calculate APR on a credit card. However, the principal formula for the APR remains what it is, so here is how you calculate APR for a mortgage, along with its formula.

APR: (((F + In) : Principal : n) x 365 (days) x 100

APR: Annual Percentage Rate

F: Total fees such as administration fees

In: Total interest paid

Principal: Total amount of loan

N: total number of days for the loan term.

To get you the idea, let’s try to calculate the total APR for example, shall we? By using this formula, for example, you are taking a loan for $2000, with the loan terms of 180 days. Then you would also pay $120 as an interest, and the lenders would also charge you $50 as an administration fee. So, here is how you calculate it.

Here is how you should do it:

- First, add the total amount of fee that has been charged, which will be $120 + $50: $170

- Now, divide the total amount of the loan by $170, so: $170: $2.000: 0.085

- Now, divided it by the total number of days for the loan/mortgage term: 0.085 : 180: 0.00047222

- Multiply it by 365 days, and you will have an annual rate: 0.00047222 x 365: 0.1723603

- Convert it into percentage by multiply it 100: 0.1723603 x 100% : 17.23%

- So, the APR for your loan/mortgage will be a 17.23% rate that you need to pay annually.

What makes it different from the mortgage loan, is there will be also many other things to consider, such as the total value of the land/property that has been mortgaged, the availability, and trust from the borrowers, etc., these also affecting on how you would calculate the total APR for the mortgage.

FAQs regarding APR

To help you better understand how APR works, and what things you need to know before taking a loan, or having an investment that has an APR, here are a few frequently asked questions regarding APR, and things to be considered when using APR for your loan.

How to know if the APR is a fair amount of rate?

The APR aims to give an exact amount of annual interest rate that is agreed upon by both sides. Before taking a loan, you will be given the exact amount of total interest and the APR that you should pay. It was calculated based on the total amount you have on a loan, the fees, and the number of days you would repay that loan.

Does APR matter if you pay on time?

Some financial institutions will have stricter time schedules when it comes to paying your loan or APR, some might be more lenient. However, when you will pay the APR will be determined, and the agreed-upon contract before is signed.

How to find the annual interest rate

To find the annual interest rate, you can find it on the contracts that will be given before you are signing a contract on a loan, mortgage, or investment. If there is any APR or just an annual interest, then it will be shown on the contract first, before you agreed on signing them.

Now, that’s the answer to the question of what is APR and how APR works for the loan, and mortgage, along with how you calculate them.