Current and prospective homeowners in the US are all eagerly watching the housing market to see what it will do over the next few years. Will there be another housing market crash? Or will the real estate market be able to weather the storms of rising inflation, higher interest rates, and an uncertain global economic climate? In what follows we will examine the impact these and various other factors will play in the US housing market over the short and medium-term and look at the most important market trends.

The US Housing Market Over The Short Term: 2023 and 2024

The CPI (consumer price index) reached its highest level in 40 years in March 2022, with prices increasing by 8.5% on an annual basis. Home prices could not escape this trend. The price of the average house increased by a whopping 17% in 2021 – the biggest increase in at least 20 years. And a recent Reuters report predicted that 2023 will bring a further 10% growth in home prices.

So are we looking at the next real estate bubble? Not if the Federal Reserve could help it. The Fed has already announced the first of several increases in interest rates, which immediately pushed up mortgage rates. The latter continues to rise, with the average rate on a 30-year fixed-rate mortgage reaching 3.8% during the first quarter of 2022 – and much worse is to come (see the relevant section below).

Freddie Mac predicts that the average rate for 2022 will be 4.6% and that it will go up to 5% next year. The Fed’s aim with these interest rate hikes is to reduce the excess demand in the housing market and thereby help keep price increases in check. As we will see later on, higher mortgage rates could, however, lead to rent increases and even higher inflation levels.

Will The Housing Market Crash Again?

Very high mortgage rates will undoubtedly have a negative impact on the real estate market because the cost of buying a home will increase. So far, however, demand for housing remains fairly strong. Many would-be homeowners are buying now in an attempt to still get a good mortgage rate before it increases again. This is one of the reasons why In 2021 home sales reached a remarkable 6.9 million, the best it’s been in 15 years.

Taking into account the recent and expected increases in mortgage rates, however, Freddie Mac predicts that home sales will start tapering off to 6.7 million for the whole of 2022 and that 2023 will see this number drop to 6.6 million. The company also expects that home prices will start growing at a slower rate of 10.4% in 2022, followed by 5% in 2023. In 2024 price growth is expected to slow down even further to 4.1%.

According to Freddie Mac’s real estate market analysis, therefore, the answer to the question: “Is the housing market about to crash?” is a definite no, at least for the short term between now and the end of 2023. The current real estate market is still solid…but as we will see later on, there are factors at play that could dramatically change the picture.

More Housing Market Trends

Over the last 10 years, the inflow of large numbers of millennials into the U.S. housing market combined with chronic housing shortages have caused a huge mismatch between demand and supply in the housing market. Despite more increases in mortgage rates, it is not expected that house prices will start falling any time soon. We can, however, expect that prices will not grow quite as fast.

The housing statistics released by Realtor.com in April 2022 showed that the median list price of homes for sale has reached a historical high. At the same time, the number of homes that were in the process of being sold did, however, started to decline.

Another issue currently affecting the housing market is that sellers have returned. This can be seen from the increase in the number of recently listed homes compared to the same time last year. In the next few months, stock levels are thus expected to increase compared to 2021. The plus side of this is that buyers should experience more options and less competition.

The Impact Of Wage Increases And Rising Prices On The Housing Market

In 2020 the Coronavirus impact hit the United States like a bomb. Many businesses had to close their door and millions of Americans were forced to stay at home – or even worse, lost their jobs. The only way the Federal Reserve could combat increasing unemployment was to improve unemployment benefits, announce a freeze on the repayment of business loans, and issue stimulus checks worth billions of dollars.

This caused the country’s savings rate to reach record levels in 2021. As the nation started to recover from the pandemic, many new jobs were created and unemployment levels started dropping.

Right now, the majority of large cities have recovered most if not all of their lost job opportunities. There are, in fact around 11 million unfilled job openings. In certain industries, there are not even enough workers to fill the available jobs. This is forcing competing employers to increase pay rates.

The downside is that these wage increases are mostly passed on to consumers in the form of higher prices. No wonder, therefore, that the inflation rate (including home prices) increased so sharply.

What has the inflation rate got to do with the housing market? If the current trend continues over the next few years it will certainly create problems for this market. If salaries and wages do not keep up with price increases, it will have a negative impact on savings. And the latter plays an important role in the demand for residential homes. Right now it’s way too early to talk about the next housing market crash, but it’s something that will have to be closely monitored by the Federal Reserve.

Is It A Good Time To Buy A House?

Polls show that fewer buyers currently believe that it’s a good time to purchase a home. Despite that, however, there are still millions of Americans who are searching for their dream home. This is particularly true in the case of first-time home buyers. Unfortunately, many of them are finding it very hard to save enough for a down payment on a home.

Under the current circumstances, it is very unlikely that the housing market will anytime soon change from a seller’s market to a buyer’s market. The fact that mortgage rates are expected to increase even further in the coming years will make things even more difficult for buyers. This could dampen demand somewhat and slow down the sharp rate of increase in home prices. It could also help to prevent the market from becoming overheated.

In the sense that right now mortgage rates might be at the best level (from a buyer’s point of view) they will be in years, one could argue that anyone who wants to buy a home should rather do it now instead of waiting another year or two. Housing inventories are already low, and this, combined with higher mortgage rates, could soon make owning a home an unrealistic dream – particularly for many first-time buyers.

Another reality is that, if home prices should continue growing at the current rate, the possibility of a real estate bubble developing could become a reality. In April 2022, for example, the median home price in Miami increased by a shocking 38.3% on an annual basis. Las Vegas notched up an increase of 32.6% and Orlando 30.7%.

Increases like these are not sustainable in the long term. The income of the average wage earner simply doesn’t go up at nearly 40% per year. Combine that with sharply increasing mortgage rates and a relatively high inflation rate and a new real estate bubble could well start forming over the next few years – with prices soaring to completely unrealistic levels.

When Will The Next Housing Market Crash Happen?

The burning question at the back of many people’s minds is how soon will we see the next housing market crash? Most experts believe that it is unlikely to happen between now and 2025, and definitely not before the end of 2023. Most current forecasts show that the market will most likely remain robust over the short term, with most of the trends that pushed up home prices to record highs last year continuing to drive the market.

During the past few years, home prices have escalated quite dramatically. Many would-be buyers are worried that if this trend continues, they might never be able to own a home. Whether this will happen or not depends mainly on two factors: the good old demand and supply.

Once demand and supply are in equilibrium, home prices will start dropping. At the moment, however, there is huge pent-up demand for residential properties and there are simply not enough available homes to meet this demand. Even though the construction of new homes has increased over the last few years, supply has still not caught up with demand. This will continue to drive prices higher until either supply catches up or demand falls.

As a general rule, demand will only start dropping if interest rates become too high for the average buyer to afford or there is a general economic slowdown. Before interest rates can have a significant impact on home prices, however, they will have to increase much more. If supply should also increase at the same time, one could get to a point where we no longer have excess demand. At that stage, home prices will first increase at a slower rate before eventually starting to drop.

The most likely scenario for the rest of 2022 and 2023 is, therefore, that the housing market will cool down somewhat, with supply slowly catching up with demand and further mortgage rate increases keeping demand in check.

Making real estate market predictions at a time like this is a bit like trying to predict the weather: A sudden change in the direction of the wind can make all your carefully compiled calculations relatively useless.

During the more than 10 years that have passed since the last economic recession, the United States economy has experienced one of its longest-ever periods of continued economic growth. The housing market has and continues to benefit significantly from this economic prosperity. Even the hottest economy will, however, sooner or later start cooling. When that happens it will undoubtedly have an effect on the housing market.

The fact is that, although housing inventory has increased somewhat, it is still significantly lower than before the pandemic and definitely doesn’t meet present demand. Combine that with an increase in demand and it’s hard to see a situation where supply will exceed demand anytime soon. Instead of a housing market crash, one should rather expect more bidding wars between buyers over the short to medium term.

What Will Happen To The Housing Market If Inflation Continues to Increase Rapidly?

If inflation continues to rise, it is virtually a given that the Federal Reserve will attempt to keep it in check by increasing interest rates, including mortgage rates. The Fed has already clearly indicated that it intends to follow an aggressive policy toward raising rates.

When higher interest rates push up the cost of borrowed money, it typically has a negative impact on consumer spending, including the demand for homes. The reverse is also true: lower interest rates make money cheaper, boost consumer spending, and increase demand in the housing market. This is why the Fed reduced interest rates so dramatically during the pandemic.

While this might have been necessary at the time, many experts believe that the Federal Reserve kept these policies in place for too long. It was only in 2022 that it started to increase interest rates again. The danger is now that it might increase these rates too much too quickly, in which case it could push the economy (including the housing market) into a recession. One warning sign is that GDP growth has already started to slow down.

Another negative spin-off is that the higher mortgage rates could deter many prospective home buyers. Depending on exactly how much interest rates go up and how quickly, this can have a hugely negative impact on the demand for homes. With more buyers out of the market, the demand for rental properties will increase. This will in turn push up rents even further – a dreadful situation to be in if you are a tenant, but very good news if you are the owner of one or more rental properties.

How Will Supply And Demand In The Housing Market Impact House Prices Over The Next Few Years?

US homebuilders are currently struggling with problems such as an inadequate supply of trained and experienced workers and supply-side disruptions because of what is happening in international markets.

Housing inventory levels have already reached historic lows and the situation is not likely to improve anytime soon. As mentioned earlier, this means that we have a classic case of demand/supply imbalance, with supply simply unable to meet demand.

Another factor that plays a role here is that the rapidly increasing input costs are encouraging those in the construction industry to focus more on expensive homes where the profit margins are higher instead of the starter homes for which there is a huge demand.

Combine this with the fact that many millennials are now for the first time looking to buy a home and it’s not difficult to see why home prices are skyrocketing.

How can this be resolved? Of course, the Fed can (and probably will) increase interest rates to curb demand. This is a rather artificial solution since the need for a roof over one’s head is a very basic one. Increasing interest rates will not eliminate that demand. It will simply build up more pent-up demand that has to be met sooner or later.

People who can’t buy a home will start looking for rental homes. This will indirectly further increase the demand for new homes because landlords would want to increase their stock of rental properties. And if the supply doesn’t increase, the additional demand for homes will further push up home prices.

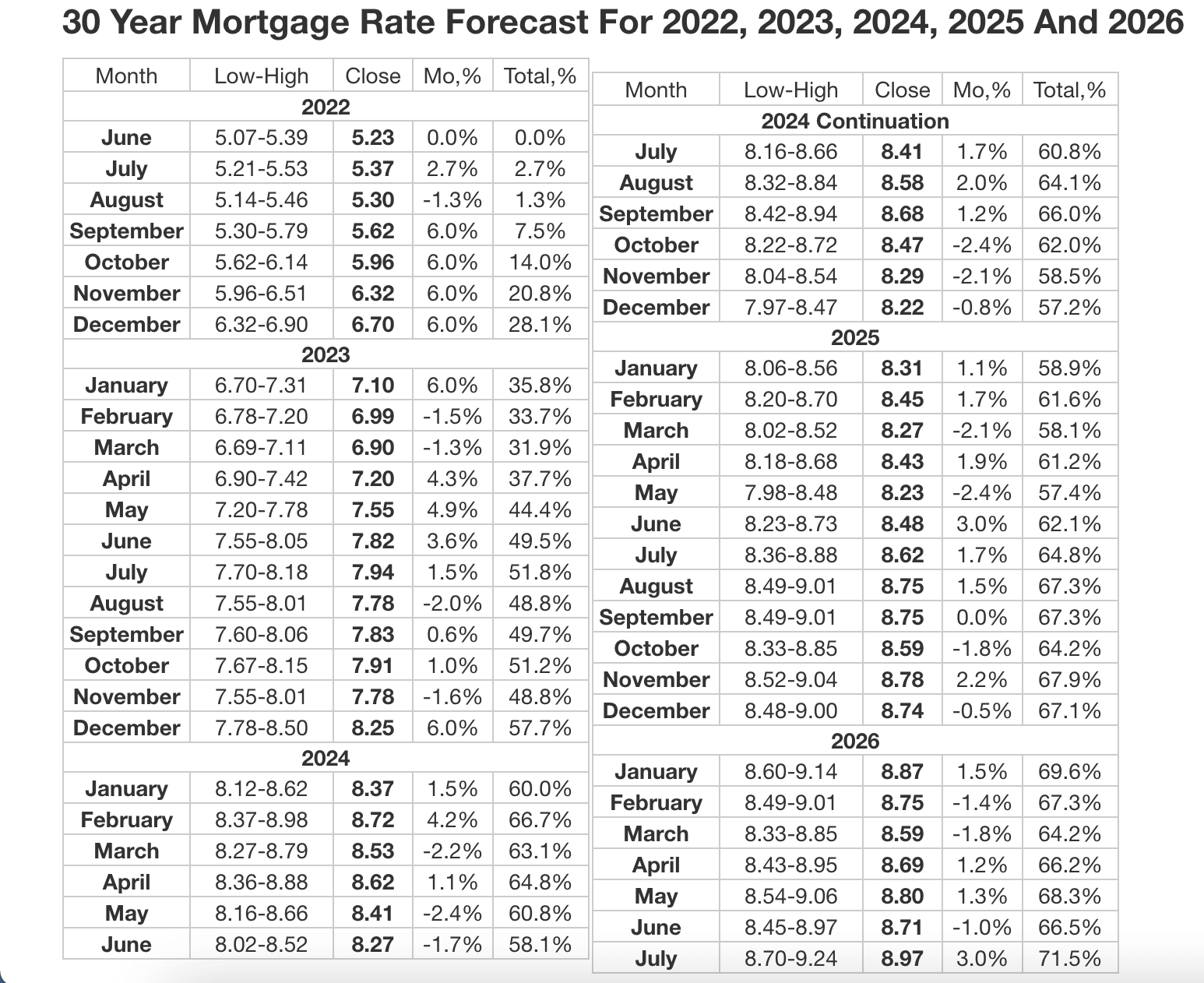

Where Will 30-Year Mortgage Rates Go Over The Next Few Years?

Whether we like it or not, mortgage rates are unlikely to come down anytime soon. According to the Longforecast.com website, the 30-year mortgage rate will be as follows between now and 2026:

2022: (July) 5.08%

2022: (December) 6.1%

2023: 8.08%

2024: 7.78%

2025: 8.7%

2026 (July): 9.70%

If these predictions should turn out to be accurate, it seems that the Fed will continue using interest rates to curb what it views as excess demand in the economy. And four years from now borrowers will pay 9.70% interest on their mortgages instead of the current 5.08%. Just to give readers an idea of what that will mean: the monthly repayment on a $100,000 mortgage will go up from $541.72 to $855.48 – a whopping 55% increase.

If that becomes a reality, the huge increases in mortgage rates will undoubtedly place further pressure on the demand for homes, making it even more difficult for younger people to afford their first home.

How Will The Demand-Supply Imbalance Affect House Prices In the Suburbs?

According to data recently released by Zillow, the biggest increases in home prices are currently seen in ‘family friendly’ neighborhoods. This can probably be ascribed to the growing impact millennials are having on the residential property market.

Between October 2020 and October 2021, the neighborhoods with the biggest share of kids on average reported a growth rate of 21%. In comparison, the rate for neighborhoods with the smallest share of kids was quite a bit lower at 17%.

Zillow ascribes this to millennials that are looking for houses that meet the needs of their growing families.

It can be expected that demand for homes in family-friendly neighborhoods will continue to grow over the next few years. This will undoubtedly put even more upward pressure on prices in these areas.

According to the same press release, Zillow’s data also shows that the impact of Millennials reaching the prime age for purchasing a home has increased over the last 9 years. The company believes that this trend will further increase over the next few years. Nearly 200,000 more millennials will reach the age of 32 this year than last year and in 2023 and 2024 the numbers will be even higher.

This effect is currently particularly strong in the following regions of the United States: Tampa, Florida; Salt Lake City, Utah: Raleigh, North Carolina: Los Angeles, California; Jacksonville, Florida; Seattle, Washington; Austin, Texas; Portland, Oregon; Virginia, Washington, D.C.; and Norfolk, Virginia.

How Will Cash Sales Affect US House Prices?

In April 2022, the percentage of homes that were sold for cash dropped from 28% to 26%. That nevertheless means close to a third of all home purchases in the US were settled in cash – an indication of the large numbers of buyers still out there who have enough cash available not to have to worry about mortgage rates. It is also an indication that higher mortgage rates might not have such a severe impact on the housing market during the short to medium term as many observers expect.

How Will Preferences In The Housing Market Change Over The Next Few Years?

In spite of the recent increases in mortgage rates, HUD and Census Bureau data show that the median price of new residential homes increased by 21.4% to $436,700 between March 2021 and March 2022. These relatively high prices are expected to continue into next year and beyond. The data also shows that, despite recent increases in mortgage rates, many home buyers are still willing and able to pay relatively high prices for their dream homes.

In the current market, demand is particularly strong for detached single-family homes and new homes. The former will most likely remain popular for many years to come because they offer more living space and privacy than their attached counterparts.

With housing costs continuing to consume an ever-increasing percentage of home buyers’ paychecks, many people will have no choice but to become very inventive. Some of them will choose to move to the suburbs where homes still cost less per square foot than their more centrally located counterparts. Prices here might grow at a slower pace – but low inventory levels and increasing demand will make sure that they remain high despite a steady increase in mortgage rates.

A fairly new trend that is virtually sure to further transform the US housing market in years to come is the significant increase in the number of people who work from home. There are currently more people who work remotely than ever before. These people have the choice to leave the city and move to the suburbs or even to a small town on the coast or in the mountains where home prices are still relatively low – for now.

This is one reason why places such as Florida are experiencing such a huge inflow of people from New York and New Jersey. Of course, over time, the increased demand for homes in these areas will definitely start pushing up real estate prices, but right now they are still significantly more affordable than most of the major cities.

How Will Developments in the US Housing Market Affect The Market For Rental Properties?

Rents across the US started increasing rapidly in 2021, with cities like Phoenix, Austin, and Miami averaging increases of more than 40% p.a. For the US as a whole the figure stood at 14%. One of the reasons is that large numbers of millennials are now getting married and starting a family. And they are all in need of a roof over their heads.

With supply shortages and rising mortgage rates driving up home prices, many of these people have no other choice than to rent. This is steadily increasing the demand for rental properties – and in turn, driving up rents.

With a limited supply of rental properties and an ever-increasing demand, it is only reasonable to assume that this situation will continue to worsen over the next few years. The only long-term solution will come when there is an equilibrium in the housing market again, with supply matching demand. Until then the excess demand in both the for sale and rental markets will continue to drive up home prices as well as rents.

How Will Developments In The Housing Market Impact Lending Requirements From Here On?

According to the MBA (Mortgage Bankers Association), the recent drop in the MCAI (Mortgage Credit Availability Index) is an indication of tightening lending standards over the short to medium term. The MBA also revealed that there was a drop in mortgage credit availability at the start of 2022.

The easiest way to pick up that there was a tightening in lending requirements is to check whether the Fed has started to reduce available credit. When the Federal Reserve starts to withdraw funds from the market, credit providers have less money to lend to borrowers. This in turn leads to banks starting to restrict their lending activities to only the most qualified borrowers.

Stricter lending requirements and higher mortgage rates eliminate large numbers of would-be buyers from the race to qualify for a home loan. This will in turn force more people to rent instead of buy. Rents will then typically start to increase – and so will the inflation rate, the one thing the Fed was trying to reduce in the first place!

Will There Be An Increase In the Number of Homeowners Who Default On Their Mortgages?

At the end of 2021, the number of properties that filed for foreclosure showed a shocking increase of 129% compared to the year before. And according to statistics released by ATTOM Data Solutions, there were 25,833 foreclosure filings.

The fact that there was a moratorium on foreclosures during the pandemic played a major role in this. One can, however, expect that the situation will not be resolved anytime soon because higher mortgage rates and rising prices are stretching US households’ budgets to their limit. Historically speaking, however, the number of foreclosures still remains relatively low and there is no sign of a developing crisis at this stage.

A lot will depend on what happens over the next few years. If mortgage rates continue to soar and inflation keeps eating away at the average American’s disposable income, more and more of them might end up defaulting on their mortgages. The ones that will get through this unscathed are those who opted for fixed mortgage rates. That is why those who chose this option are currently so reluctant to sell their homes: they are locked into fairly low interest rates – a great position to be in during a time of increasing mortgage rates.

Final Housing Market Prediction For The Next Few Years

In March this year, the CPI (Consumer Price Index) showed that inflation has reached 8.5% – the highest rate in four decades. Despite the Fed’s attempts to curb further price increases, it is not reasonable to assume that the situation will be completely resolved anytime soon.

This means that investors will continue to put their money in inflationary assets like real estate. In an economy where inflation is a reality, borrowers are the winners since they can repay their debt with money that has lost a significant part of its value. This is why real estate has for many years been regarded as such a strong hedge against inflation.

Savvy investors are actually banking on inflation, which is why they buy assets like real estate that often increase in value faster than the inflation rate. With property values currently increasing at more than 10% p.a. and mortgage rates still relatively low (although increasing), returns on these investments are expected to remain excellent over the next couple of years. This is why so many institutional investors are buying real estate right now.

The bottom line is that, despite its ups and downs, the housing market will remain a solid hedge against inflation and other economic storms in years to come. We don’t foresee anything similar to the Great Recession happening again over the next few years. And with the information currently at our disposal, we definitely don’t see the housing market heading for a crash over the short to medium term.

If house prices, however, continue to increase faster than incomes and available inventory becomes even tighter across the United States, no housing market 10-year forecast could totally eliminate this possibility…

Sources:

https://www.freddiemac.com/research/forecast/20220418-quarterly-forecast-purchase-market-will-remain-solid-even-mortgage-rates-rise

https://www.eastatlhomebuyers.com/blog/when-will-the-housing-market-crash-predictions/

https://www.reuters.com/business/us-house-prices-rise-another-10-this-year-2022-03-02/

https://realwealth.com/learn/housing-market-predictions/

https://www.mordorintelligence.com/industry-reports/residential-real-estate-market-in-usa

https://longforecast.com/mortgage-interest-rates-forecast-2017-2018-2019-2020-2021-30-year-15-year